A "Deductible" is the amount of money you, the policyholder, are responsible for paying out-of-pocket before your insurance company begins to pay for a covered loss.

Let's break down what a deductible is! Think of your deductible as your personal co-pay for a covered loss. It's the first bit of money that comes out of your, the policyholder’s, pocket when you make a claim before your insurance company steps in to cover the rest.

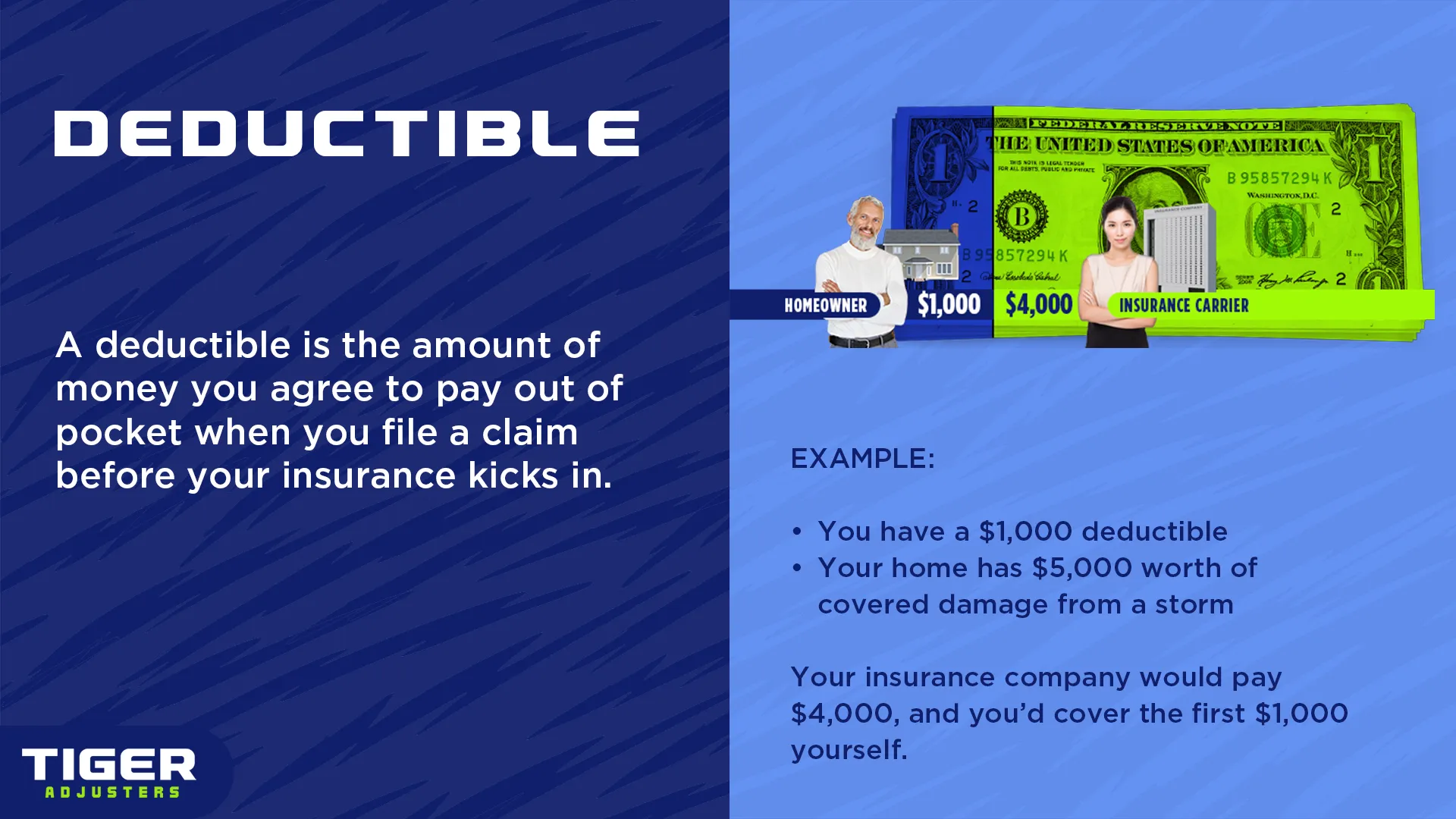

Here's how it generally works: Let's say you have a homeowner's policy with a $1,000 deductible. If your roof gets damaged in a storm and the repair cost is $10,000, you'd pay the first $1,000, and then your insurance company would pay the remaining $9,000. It's essentially your share of the risk.

While most property and casualty insurance policies, like auto and homeowner's, have deductibles, there are exceptions. Some policies, or specific coverages within a policy, might not have a deductible. For instance, liability coverage in an auto policy typically doesn't have a deductible, as it covers damages you cause to others. Similarly, certain medical insurance plans might have co-pays or co-insurance instead of a traditional deductible, or even no deductible at all for specific preventative services. However, for anything related to repairing your own property or significant medical procedures, a deductible is almost always a factor.

No, they are definitely not! The type, amount, and how they apply can vary significantly between policies and even within different sections of the same policy. For example, your homeowner's policy might have a standard deductible for fire damage, but a separate, higher percentage deductible specifically for wind or hurricane damage. Auto policies often have separate deductibles for collision versus comprehensive coverage. It's crucial to understand each deductible in your policy, as a higher deductible means less upfront cost in premiums but more out-of-pocket expense if you make a claim. Always compare deductible options with your premium savings to verify it aligns with your financial comfort level and risk tolerance.

Your insurance deductible is more than just a number; it's a key factor in your insurance costs and financial readiness for a claim. Understanding your deductible—how it works and its implications—is vital for making informed decisions about your coverage. Don't let confusion about deductibles leave you exposed; review your policy thoroughly and if you're ever unsure about your responsibilities during a claim, especially regarding the deductible, reach out to your Public Adjuster.