This underscores just how important it is to have your policy precisely tailored to avoid those gaps!

Endorsement Purpose

Think of your standard insurance policy as a basic warranty. It covers the common stuff, but sometimes you have unique items that need extra care. That’s where endorsements, sometimes called "riders," come in. This is your way of upgrading your financial protection, letting you fine-tune your coverage against specific threats or for special possessions, like a Rolex watch. It helps you fill in the gaps where a regular policy might leave you exposed. Endorsements can be added at any time to modify the existing property insurance policy.

What an Endorsement Does:

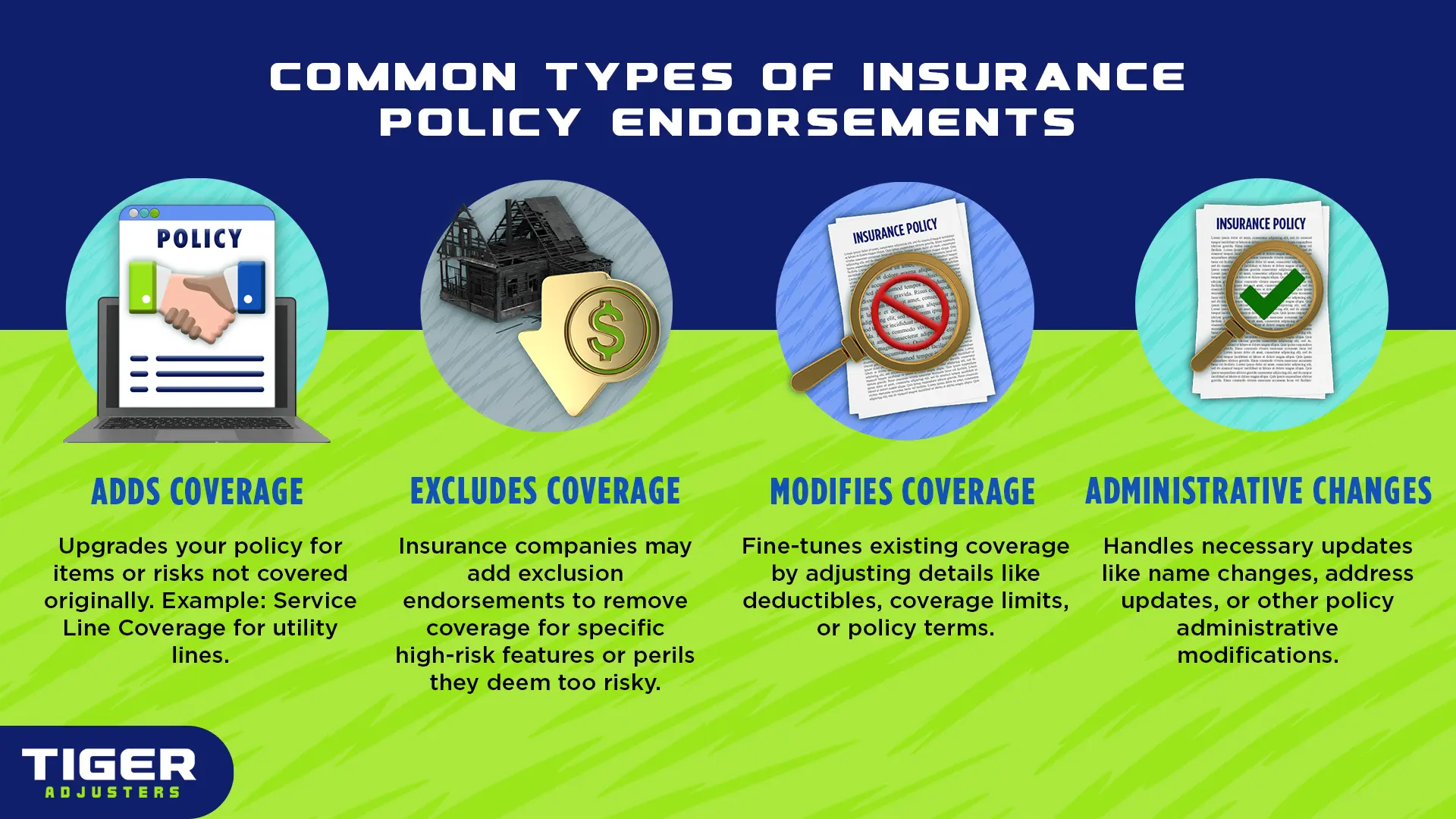

Adds or Increases Coverage: This is your upgrade for items or risks not covered by the original policy, or it can increase the limits of existing protection.

Excludes Coverage: Sometimes, an endorsement is used by the insurance company to specifically remove coverage for certain perils or types of losses. It’s important to read the fine print.

Modifies Coverage: Your insurance company can fine-tune your existing coverage, adjusting details like your deductible or who is covered under the policy.

Administrative Changes: Endorsements can also handle mundane but necessary updates, like a name change or a new address.

How an Endorsement Works

First, identify a specific need or exposure that isn't properly addressed by your current policy's default settings.

Then, submit a request to your carrier outlining the desired change or addition to your coverage.

Once approved, the endorsement is added to your policy document, effectively overwriting or appending specific clauses, initiating the updated coverage.

This creates a tailored insurance solution, making sure your financial defenses are protecting your valuables.

Infographic: Common Types of Insurance Policy Endorsements

Does Insurance Always Require an Endorsement?

Not every minor tweak requires a formal endorsement; sometimes policy updates happen quietly in the background. But when you need to specifically add or subtract substantial coverage, or redefine policy terms, an endorsement is the standard protocol for making that change official. But note, carriers can sometimes be as resistant to change, and the process can involve a bit of back-and-forth, especially if your request is unusual or complex.

Breakdown of Endorsement Scenarios:

Scheduled Personal Property Endorsement (Policyholder-Initiated)

This is your high-value asset protection module. It allows you to list specific items that exceed standard personal property coverage limits.

Provides individual, often "all-risk" coverage for these items, safeguarding them against perils typically excluded or limited in a standard policy.

This allows these unique assets to be insured for their appraised value, rather than a depreciated cash value, preventing a data loss event for your most prized possessions.

Service Line Coverage Endorsement (Policyholder-Initiated)

Think of this as an infrastructure protection patch. Standard policies often stop at your home's foundation when it comes to utility lines.

Covers damage to underground service lines (water, sewer, power, internet) that run from the street to your home, often due to wear and tear, tree roots, or other non-covered perils. This endorsement acknowledges that even your off-property utility connections need protection from unexpected failures.

In the digital age, this is your crucial cybersecurity add-on. Standard policies don't typically cover the financial aftermath of identity theft.

Covers expenses incurred from identity restoration, such as legal fees, lost wages from time off work to resolve issues, and costs associated with notarizing documents or sending certified mail, and provides a recovery pathway when your personal data security is compromised.

Water Backup and Sump Overflow Endorsement (Policyholder-Initiated)

This is a critical flood-related patch for non-flood events. Standard policies often exclude water damage from sewer backups or sump pump failures.

Extends coverage to include damage caused by water that backs up through sewers or drains, or overflows from a sump pump.

Protects against a common, costly vulnerability not typically covered by your base policy, so that your internal water systems don't become your personal disaster zone.

Exclusion Endorsement (Company-Initiated)

Sometimes, an insurance company will add an exclusion endorsement to your policy. This is typically done to remove coverage for a specific risk they think is too high for a particular property or location.

Example: If your property has a unique, high-risk feature, like a poorly maintained, very old outbuilding, the insurer might add an endorsement to specifically exclude that structure from coverage, protecting themselves from excessive liability.

Loss Payee Endorsement (Company or Policyholder-Initiated)

This endorsement is often required when there's another party with a financial interest in your insured property, such as a lender or lienholder.

Example: When you get a mortgage, your bank will likely require a Loss Payee Endorsement. This means if there's a covered loss to your home, the insurance payout will first go to the bank to make sure their loan is protected before any remaining funds go to you.

Are All Endorsements Created Equal?

While endorsements offer customization, it's important to understand their specific parameters. Not all endorsements cover every scenario, and some may have sub-limits or unique exclusions.

Just like trying to figure out a new software update, always review the specific language of each endorsement. Don't just assume!

Getting an endorsement for that fancy new piece of jewelry doesn't suddenly mean your entire home is now covered for every single risk you can possibly imagine. Nope, it's typically just for those specific items or particular problems.

Endorsements are great for closing certain little gaps; they definitely don't magically transform your policy into some kind of "all-risk, no-exclusions" super-policy! For example, a water backup endorsement still won't cover a full-blown flood – that's a whole other beast.

Final Thought:

Endorsements are your policy's agile development feature, allowing you to tailor coverage to your unique risk profile. While they give you crucial protection, remember to really dig into each addition like you're a seasoned cybersecurity analyst trying to spot a hidden bug. For the best setup, and so you're not left exposed by some subtle policy exclusion, always give your Public Adjuster a call. We're pros at debugging those coverage intricacies!