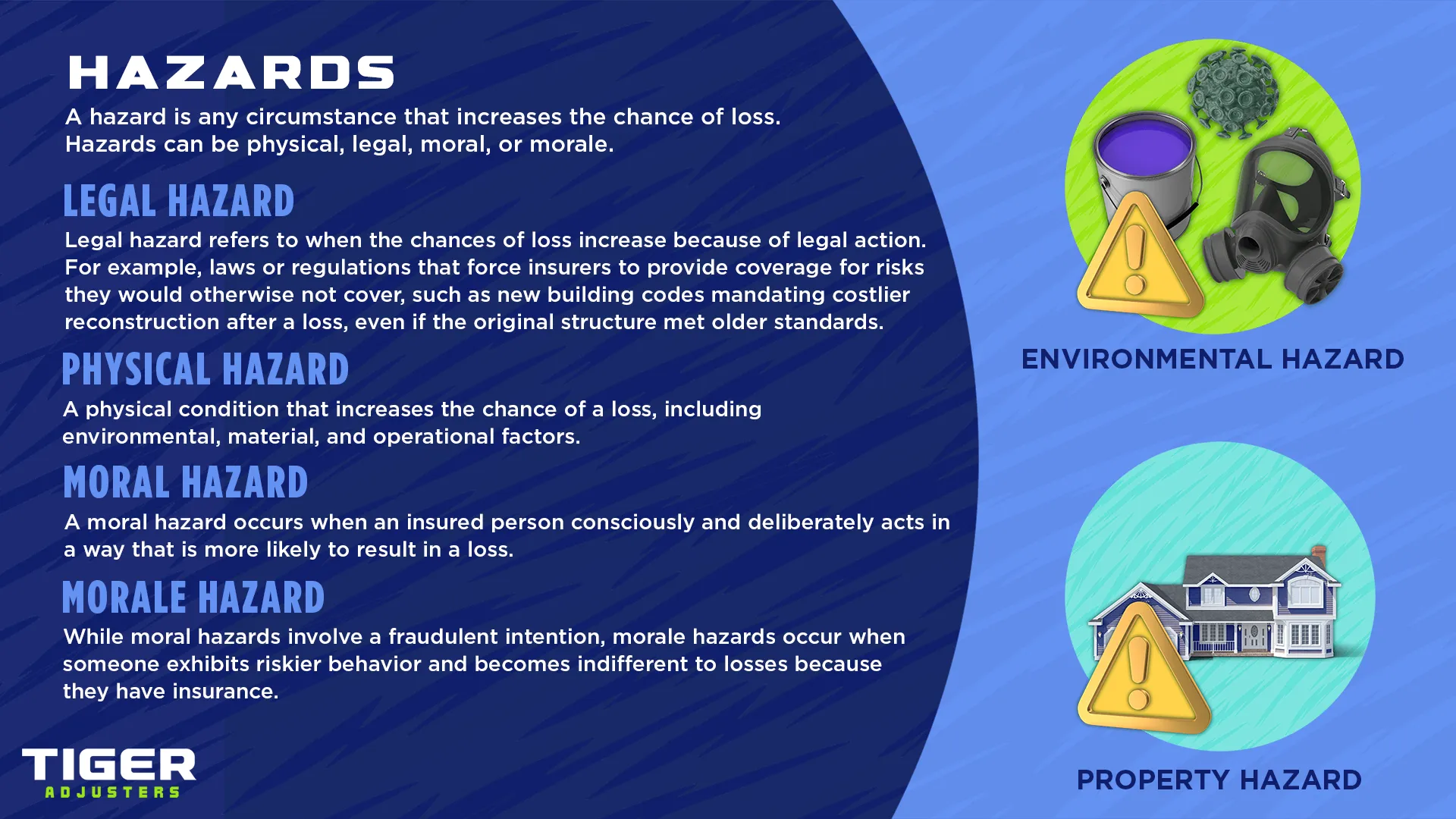

Within property insurance, a "hazard" is a circumstance, condition, or activity that increases the likelihood or severity of a loss occurring due to a covered peril. It's not the actual event causing damage (that's a peril), but rather something that makes a peril more probable or its damage worse.

Let's talk about "Hazards!" A hazard in insurance isn't the actual bad thing that happens – that's a peril, like a fire or a storm. Instead, a hazard is anything that makes that peril more likely to happen, or makes the damage from it even worse!

Think of it like this: if fire is the peril, then leaving a gas can sitting out in the hot sun on your porch is a hazard – it's just asking for trouble! Or if a car accident is the peril, then your squeaking brakes? Total hazard! It’s about spotting the little problems that can lead to big headaches.

Good news is, your policy mostly cares about hazards that are within your control or that you should reasonably know about. They want you to keep your property safe!

Bad news? If you ignore obvious hazards, or create new ones, it can definitely cause problems for your coverage down the line. Sometimes, policies even have specific clauses about maintaining your property to avoid increasing hazards. Good thing you can call a Public Adjuster to act as your property risk analyst, helping you identify potential hazards and understand how they might impact your coverage, so you’re always prepared!

No, definitely not! Insurers assess hazards based on their potential impact on the frequency and severity of losses. A small, easily fixed hazard (like a loose railing) is way less impactful than a major structural issue (like a collapsing foundation). Hazards that are within your control (like clearing dead trees or fixing faulty appliances) are seen differently than those totally outside your control (like living in an earthquake zone). Plus, your policy might have specific clauses or extra add-ons related to certain hazards, especially for things like pools, trampolines, or certain dog breeds, which might need special safety measures or additional premiums.

Hazards are the silent saboteurs that can make your worst insurance nightmares come true. Don't just wait for a peril to happen; actively identify and mitigate the hazards on your property to protect your home and your policy. For a thorough assessment of your property's hidden risks and to confirm that your preventative measures align with your coverage, call a Public Adjuster, your expert at untangling coverage intricacies who will clarify what's actually covered in your policy.