Within property insurance, "Law and Ordinance coverage" is an additional provision that helps pay for the increased costs of repairing or rebuilding your property after a covered loss, specifically when those costs are due to updated building codes, ordinances, or zoning laws. It bridges the gap between your property's value before a loss and the increased expenses incurred to bring it up to current legal standards.

When your house faces a major hit from a covered peril, your standard policy might rebuild it to old standards, but sometimes those local building codes sneak in new rules. That's where Law and Ordinance coverage steps in, kinda like an important update that makes sure your rebuild isn't just back to normal, but actually meets all the new legal standards. Think of it as your policy's built-in "compliance officer," providing that extra buffer so you're not left scrambling for unexpected costs.

Water damage and freezing accounted for 27.6% of homeowners insurance losses in 2022 (Insurance Information Institute). If a widespread event like that hits, you can bet local authorities will be looking at what's built to code, making this coverage incredibly important!

Sometimes, a basic amount of Law and Ordinance coverage (often around 10% of your dwelling coverage) might be included in a standard homeowner's policy. But here’s the kicker: that basic amount is often nowhere near enough to cover the actual costs of bringing an older property up to current codes, especially after significant damage. Insurance companies love to give you a taste, then hit you with the full bill when you're desperate.

Good thing you have a Public Adjuster to act as your chief compliance officer, auditing those code requirements and ensuring you get every cent you need!

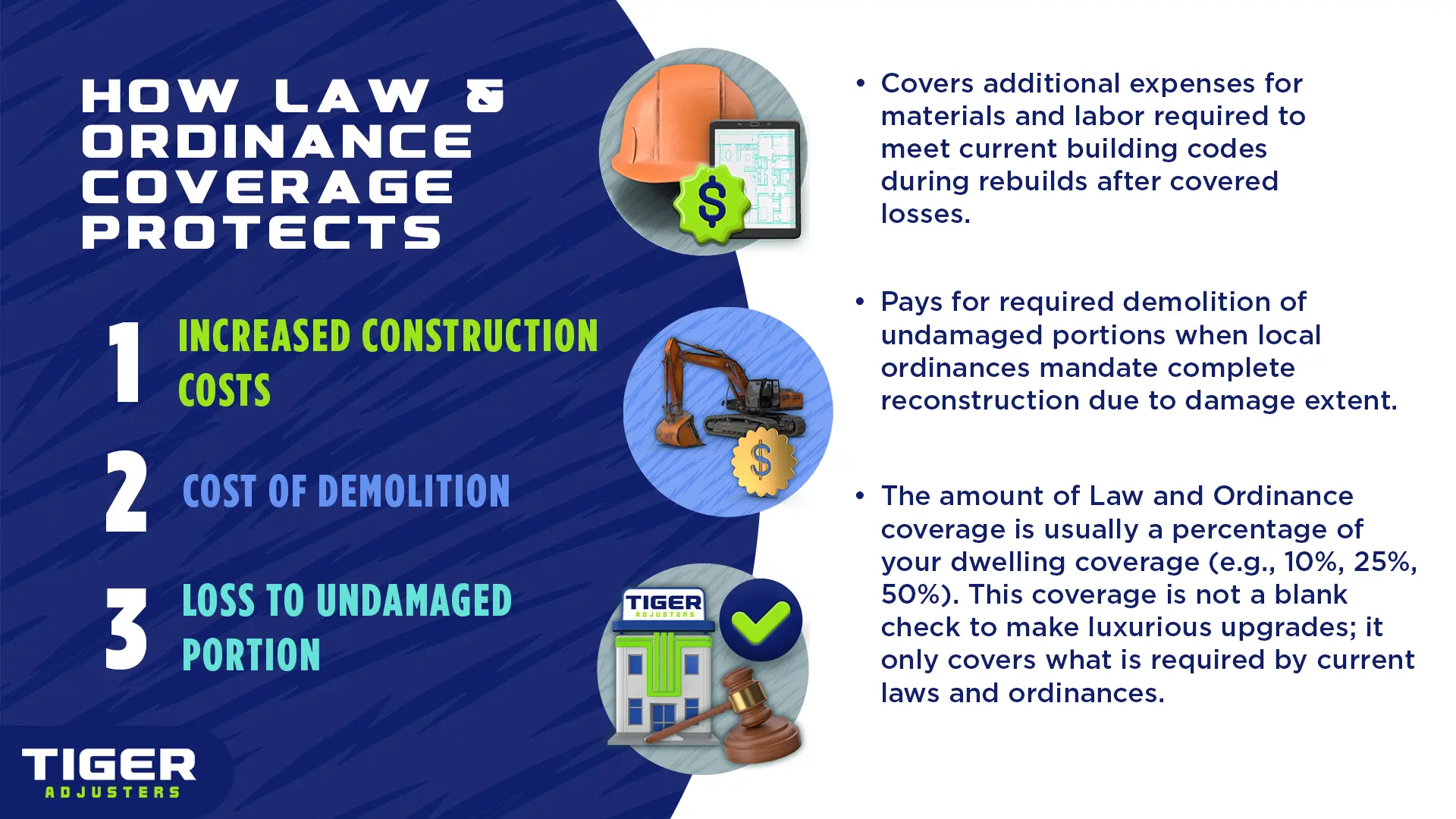

Nope, and this is where the fine print becomes your most critical piece of debugging. The amount of Law and Ordinance coverage is usually a percentage of your dwelling coverage (e.g., 10%, 25%, 50%). This coverage is not a blank check to make luxurious upgrades; it only covers what is required by current laws and ordinances.

Law and Ordinance coverage is a safeguard against the hidden costs of rebuilding your property to current legal standards after a loss. Don't assume your basic dwelling coverage will cover these essential upgrades. For a thorough understanding of your policy's Law and Ordinance limits and to verify your rebuild is fully funded to meet all legal requirements, call a Public Adjuster, who excels at debugging coverage intricacies and will clarify what's actually covered in your policy.