Within property insurance, "loss of use coverage" is the part of a policy that provides benefits when a policyholder can't live in their home or operate their business due to a covered peril.

Troy Tiger Explains: Loss of Use Coverage

Let's talk about loss of use coverage, because no one wants to be homeless after a fire! If you cannot live in your home due to fire and smoke damage, you’ve lost the use of your home. Now you have to live in a hotel until your home is rebuilt. Who covers the hotel bills? Enter Loss of Use insurance coverage.

Loss of Use coverage isn't just some fancy add-on to your policy; it's the component of your property insurance policy that comes into play when a covered peril renders your property uninhabitable or unusable. And get this: in 2022, 5.5 percent of insured homes experienced a claim, so this isn't just a theoretical worry (Insurance Information Institute)!

Think of it as the policy's built-in "get living expenses covered" card for your living situation or business operations. Loss of Use coverage provides a financial buffer against the direct impact of property damage. It covers additional living expenses (ALE) – like your hotel stays, takeout meals, laundry services – basically, all the stuff you're forced to spend money on because the covered catastrophic event decided to relocate you.

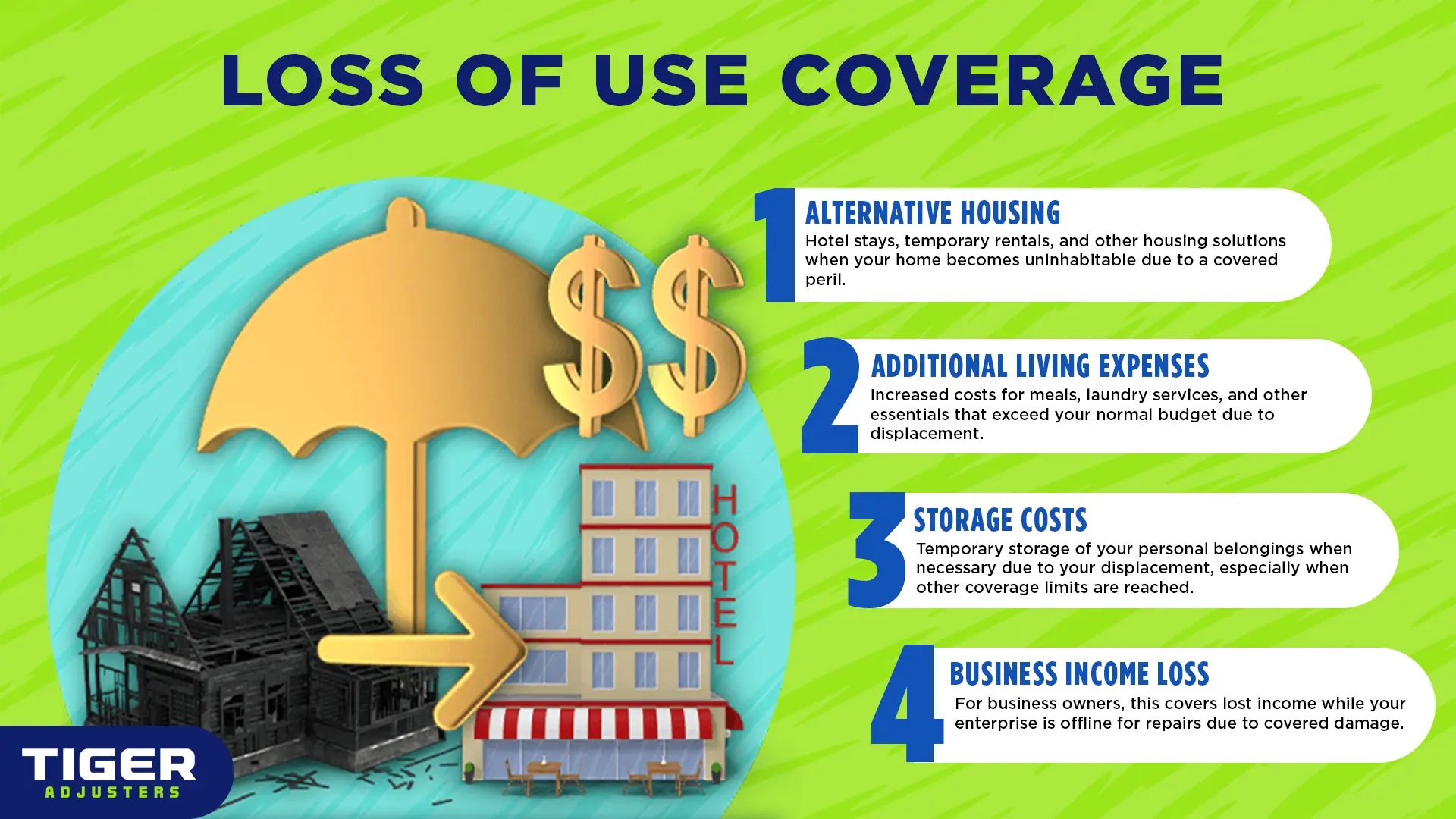

For businesses, it's about covering lost income while your enterprise is offline for repairs. It's about validating your continuity of operations, even when your building looks like it was used as a scratching post by a cat-4 hurricane.

How Loss and Use Coverage Works

First, a covered peril (damage event) renders your property temporarily uninhabitable or unusable, kicking off the process. Learn more about perils here.

Once the damage assessment is complete (think of it as a system diagnostic), your policy's loss of use component deploys, and your insurance carrier initiates financial support (i.e. checks!).

The Additional Living Expenses (ALE) funds provides you a means of covering your additional living expenses or lost business income, acting as a real-time financial patch while your primary building or home is undergoing repairs or being rebuilt.

The objective is a swift return to your pre-event operational status, minimizing downtime and maximizing your peace of mind.

Does Property Insurance Cover Loss of Use Coverage?

Good news! Loss of Use is typically covered under its own dedicated section, often referred to as "Coverage D" or "Additional Living Expenses (ALE)" within your homeowner's or renter's insurance policy.

Bad news? While it's generally included, insurance companies still manage to complicate things with their affinity for documentation. So, expect the usual bureaucratic ping-pong. Good thing you have a Public Adjuster to act as your advocate, optimizing your claims process and cutting through the noise!

This is the core protocol of your policy that activates when a covered peril renders your primary residence or business location functionally offline. It covers your system's temporary relocation expenses, such as:

Alternative Accommodations: Hotel stays, temporary rentals, or other housing solutions when your home is uninhabitable.

Increased Living Costs: Meals, laundry services, and other essential expenses that exceed your normal budget due to displacement.

Data Storage (aka, Your Stuff): In some instances, this coverage can include the cost of storing your personal property if it's necessary due to your displacement, especially if your Personal Property Coverage (Coverage C) has reached its limits or doesn't explicitly cover off-site storage in this scenario.

While not directly "loss of use," these coverages are the precursors that trigger Loss of Use. If your dwelling (Coverage A) or other structures (Coverage B) suffer damage from a covered event, leading to your property being unusable, then Coverage D comes into play. Think of them as the hardware failure that prompts the software's recovery protocol.

This component covers the value of your personal belongings themselves, rather than the expenses of your displacement. While not directly Loss of Use, there's an important interplay:

Interdependent Functionality: If your belongings are extensively damaged and unsalvageable, leading to a "total loss" scenario, the focus shifts to replacement costs under Coverage C. In such cases, the need for extensive Loss of Use storage might be superseded by a direct settlement for your items.

This clause is less about your temporary living situation and more about the cleanup post-disaster. If your property and personal items are unsalvageable, this part of your policy covers the computational resources needed for their disposal. It's the "delete" function for what cannot be recovered.

Does Insurance Cover Everything?

This is the million-dollar question, isn't it? And like most things in insurance, the answer is a resounding "it depends." When it comes to your Loss of Use coverage, here’s the high-level data stream on what usually gets processed and what hits a firewall:

Covered Perils: If your home becomes uninhabitable due to perils typically covered by your standard policy—think fire, sudden and accidental water damage (like a burst pipe, not your leaky faucet from 2008), smoke damage, or even a sudden, covered mold event—then your Loss of Use coverage is likely to activate. It's the expected system response to a documented incident.

Excluded Perils: Standard policies, and by extension your Loss of Use coverage, do not cover damage from floods or earthquakes unless you've proactively secured separate, specialized policies for those specific threats. We can't stress this enough: assume these are not covered by default.

Mold (Conditional Approval): Mold is tricky. If the mold is a direct and sudden result of a covered peril (like a burst pipe that caused water damage, which then led to mold), your Loss of Use might kick in. However, if it's the result of long-term, systemic issues or "years of neglect,” then prepare for a significant denial.

Final Thought:

If a covered event displaces you, Loss of Use coverage helps stabilize your financial bandwidth by covering additional expenses, not your regular bills. Don't assume your policy's a seamless safety net; for accurate interpretation and full utilization, bypass the carrier's labyrinthine processes and connect with a Public Adjuster, who'll clarify what's covered in your policy.