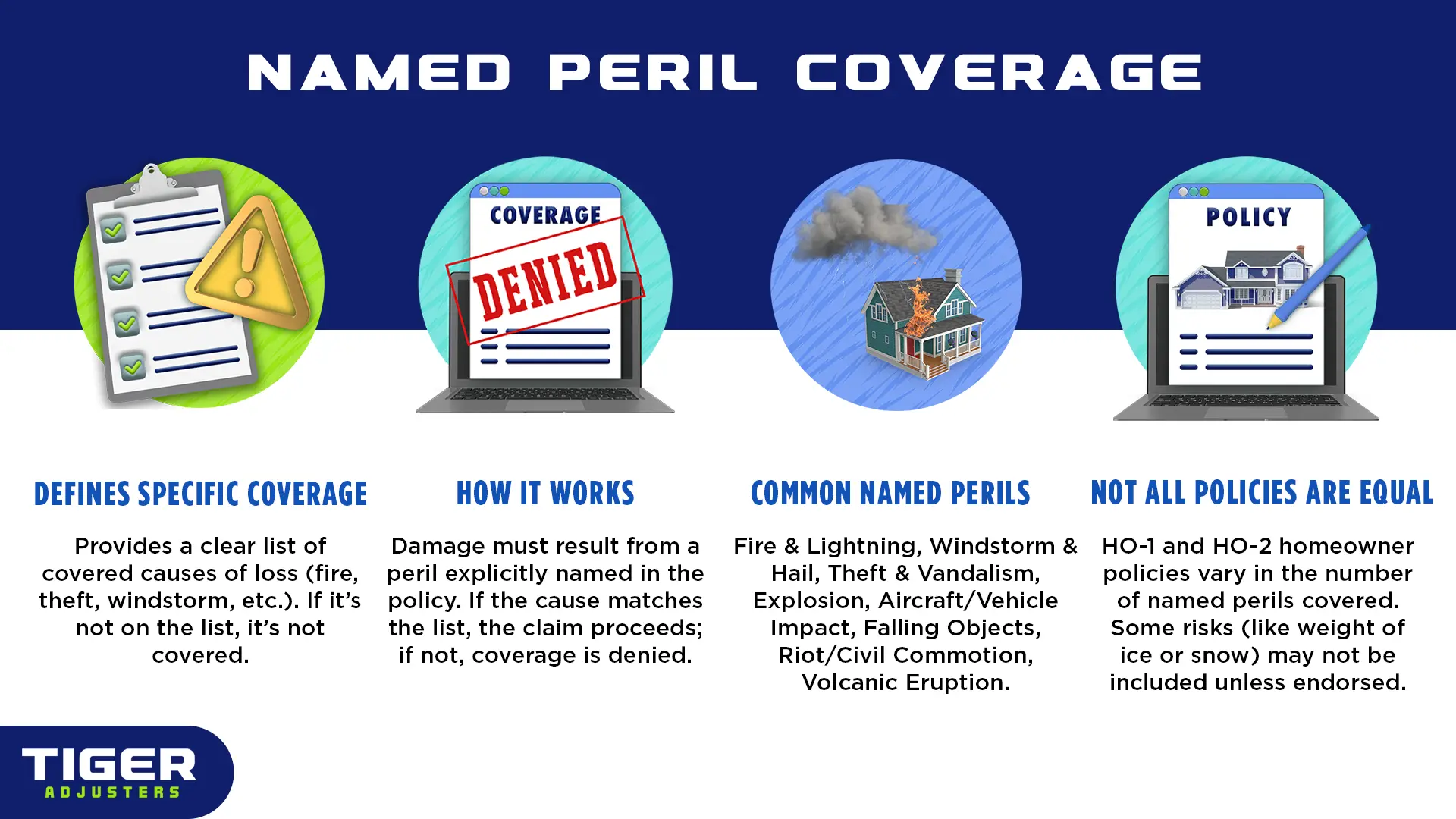

Within property insurance, a "named peril" policy explicitly lists the specific events or causes of loss that are covered. If a cause of damage is not on this list, it is not covered. This is distinct from "open peril" or "all-risk" policies, which cover all perils unless specifically excluded.

Let's dive into "Named Perils!" This sounds a bit like a secret agent file, doesn't it? But really, it’s super important. With a "named peril" policy, your insurance isn't covering everything; it's only covering the specific events that are explicitly listed in your policy. Think of it like a very strict guest list for a party – if your disaster isn't on the list, it's not getting in! If that specific cause of damage isn't written down, well, then it's just not covered. Consider this: In 2024 alone, there were 17 severe storm events, 5 tropical cyclone events, and 2 winter storm events that each caused over $1 billion in damages. This highlights the number of specific "perils" that can strike, making it crucial to know exactly which ones your policy explicitly covers!

Good news and bad news here! Most basic homeowner's policies (like an HO-1 or HO-2) are written on a named peril basis for your dwelling and other structures. Bad news? For your personal property (your stuff inside the house), policies are often "open peril" or "all-risk," meaning everything's covered unless it's specifically excluded. Confusing, right? Good thing you have a Public Adjuster to act as your policy interpreter, translating that tricky legalese and making sure you know exactly what perils your property is actually protected from!

No, they definitely aren't. Even within named peril policies, the list of perils can vary significantly, especially across different policy forms. An HO-1 policy covers fewer named perils than an HO-2. Always check the specific list in your policy. Don't just assume it's included.

Unlike open peril policies, there's no "all risks, unless excluded" clause. If it's not on the list, it's simply not covered. This means something like damage from a sudden, heavy accumulation of ice or snow (not due to wind) might not be covered if "weight of ice, snow, or sleet" isn't specifically named. However, sometimes, you can add endorsements to a named peril policy to cover additional perils not originally on the list, giving you a bit more flexibility.

Named peril policies are all about clarity – what's listed is covered, what isn't, well, isn't. While they can be more affordable, understanding that precise list is absolutely critical. Don't let a missing item on the list turn your claim into a denial. For a thorough understanding of your policy's covered perils and to confirm your protection aligns with your actual risks, always consult with a Public Adjuster. We're pros at interpreting those tricky policy intricacies and we'll clarify what's covered versus what's not in your policy!