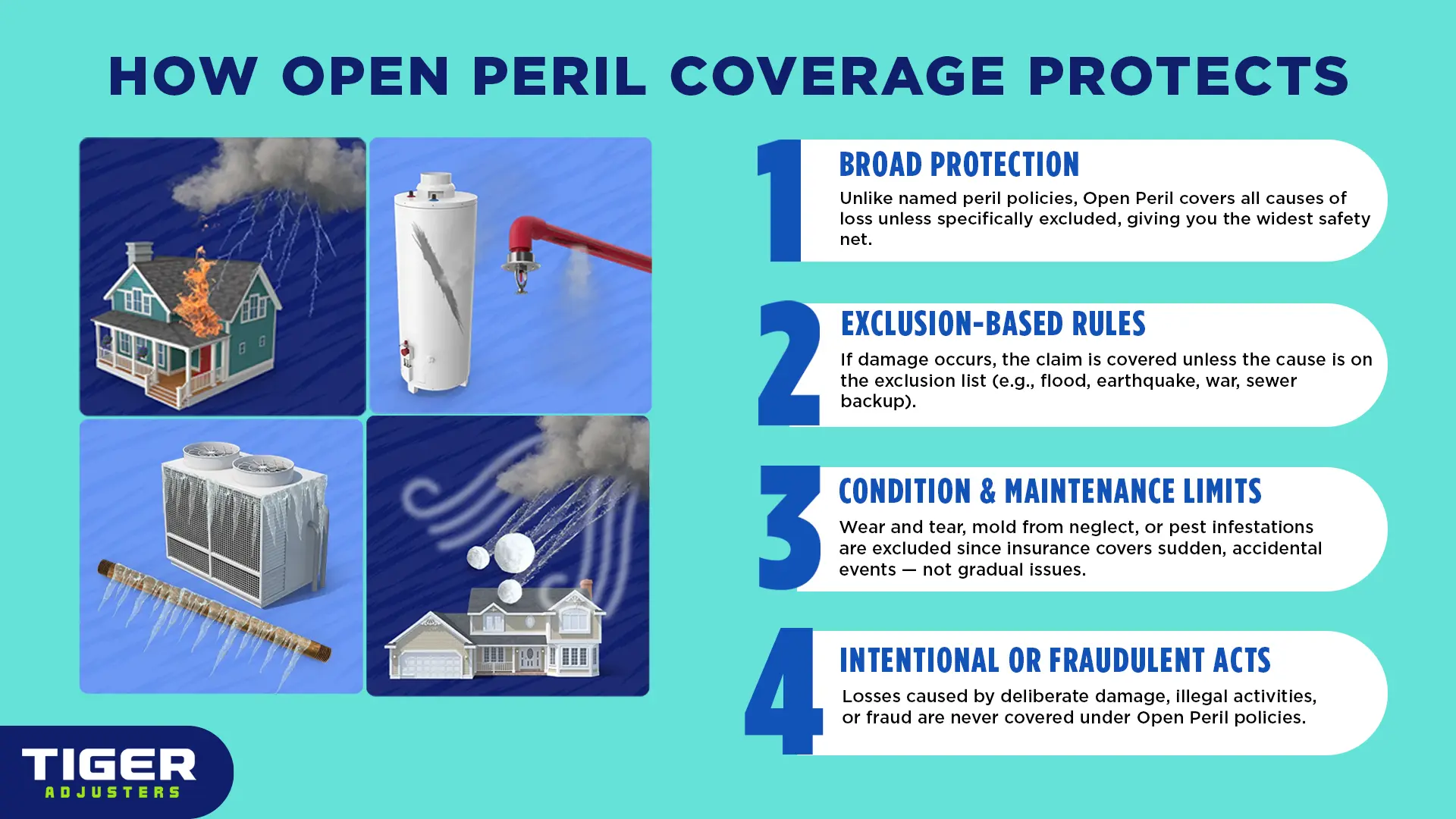

Within property insurance, an "open peril" policy (often referred to as "all-risk") covers all causes of loss unless they are specifically excluded in the insurance policy. This is the broadest form of coverage available, as opposed to "named peril" policies which only cover what is listed.

Let's talk about "Open Peril!" Now this is my kind of policy – more coverage! Unlike "Named Peril" where we're looking at a strict guest list, "Open Peril" is like saying, "Everyone's invited, unless they're explicitly banned!" It covers all causes of loss, automatically, unless that specific cause is written in the policy as an exclusion. So, if a weird, unexpected disaster happens and it's not on the "don't cover this" list, then guess what? It's covered! With 27 individual weather and climate disasters causing over $1 billion in damages in 2024, including severe storms, tropical cyclones, and winter storms, an open peril policy offers broad protection against a vast array of potential events, unless specifically excluded.

Good news! Many modern homeowner's policies (like an HO-3 or HO-5) are written on an "open peril" basis for your dwelling and other structures. So, for the actual buildings, this comprehensive coverage is pretty common!

Even better news? For your personal property (your stuff inside the house), HO-3 policies usually cover it on a "named peril" basis, but HO-5 policies generally cover personal property on an "open peril" basis too!

Even with open peril coverage, certain catastrophic or uninsurable events are almost universally excluded.

These relate to how damage occurs or the state of the property.

No, and this is where things can still get tricky, even with broad coverage. While open peril policies are designed to be comprehensive, the list of exclusions can vary between different insurers and policy forms.

Always review the specific exclusion list in your policy. One insurer's "open peril" might exclude something another covers. Even if a peril isn't excluded, it might have a sub-limit (e.g., jewelry theft). Also, some commonly excluded perils (like sewer backup) can often be "bought back" with an endorsement. Sometimes, the wording of an exclusion can be interpreted differently, leading to disputes. This is where a Public Adjuster really comes in handy!

Open peril policies offer the broadest scope of protection, covering everything unless specifically excluded. This means less guesswork for you, but it's absolutely critical to understand that exclusion list thoroughly. Don't let a hidden exclusion catch you off guard when a claim arises. For a complete understanding of your policy's limitations and to confirm your comprehensive protection aligns with your actual risks, consult with a Public Adjuster. We're pros at interpreting those tricky policy intricacies and we'll clarify what's covered versus what's not in your policy!