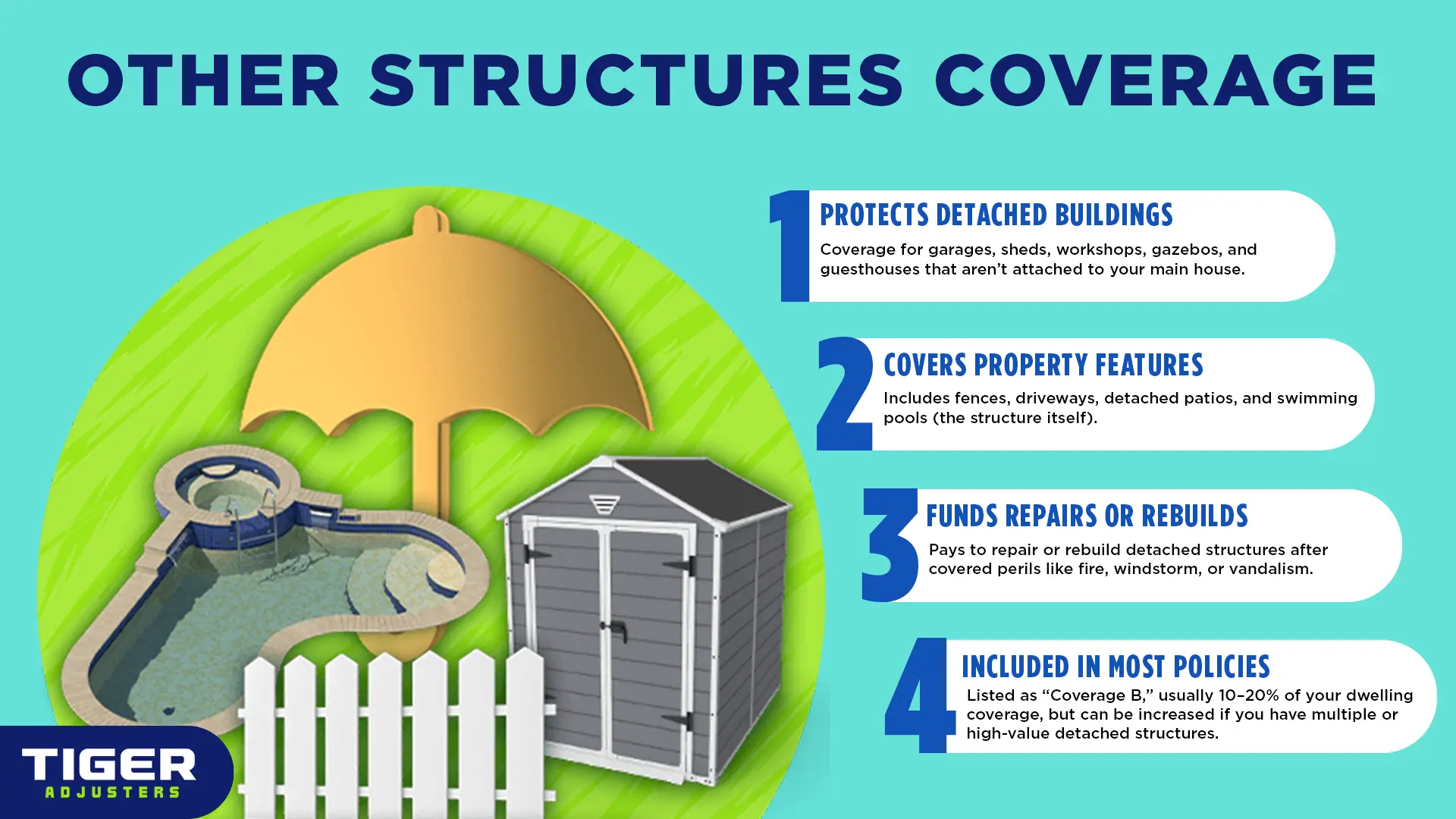

Within property insurance, "Other Structures coverage" (often referred to as Coverage B) is the part of your homeowner's policy that protects detached structures on your property, like a shed, fence, or detached garage, from covered perils. It’s the essential protection for everything on your land that isn't your main house.

Let's talk about Other Structures coverage! So, you've got your main house, right? That's your Dwelling Coverage taking care of the big boss. But what about that awesome detached garage where you tinker, or that sturdy fence keeping your dog (or tiger) in the yard, or that sweet gazebo where you relax? That's where "Other Structures" comes in, and it's pretty darn important! It's the part of your property insurance that covers all those standalone buildings and features on your land. Think of it as your home's sidekick, the essential backup system for everything else that keeps your property functional and looking good, because nobody wants their prized shed to look like it lost a wrestling match with a tornado. In 2024, the national average for all insurers combined is around 42% of property damage claims closed without payment. This highlights just how crucial it is to insure ALL your structures, not just your main house, to avoid being one of those unpaid claims!

If you have a homeowner's insurance policy, Other Structures Coverage is almost always included. It's typically listed as "Coverage B" and is usually set as a percentage of your Dwelling Coverage (often 10% to 20%).

Now, here’s where you have to be careful. That percentage might not be nearly enough if you have a really expensive detached garage or multiple valuable outbuildings. A 10% limit on a $300,000 house means only $30,000 for all your other structures combined. Good thing you have a Public Adjuster to act as your property valuation expert, helping accurately assess the true replacement cost of all your separate structures and making sure your coverage is fully utilized.

No, and this is where understanding your specific needs is crucial. The percentage of Dwelling Coverage allocated to Other Structures varies by policy and insurer. If you have multiple or very expensive detached structures, the standard 10% or 20% of your dwelling coverage might be insufficient. You might need to increase this limit with an endorsement.

Just like with your main dwelling, certain perils (like floods or earthquakes) are typically excluded from Other Structures coverage and require separate policies. Some policies might have limitations if a detached structure is used for a home-based business, potentially requiring a separate business policy or endorsement.

Other Structures Coverage is important for all those valuable buildings and features on your property that aren't your main house. Don't assume the standard percentage is enough for your specific needs, especially if you have a lavish shed or a detached "man cave." For an accurate assessment of your property's auxiliary assets and to confirm your Other Structures coverage is robust enough for any scenario, always consult with a Public Adjuster, who excels at untangling coverage intricacies and will clarify what's actually covered in your policy.