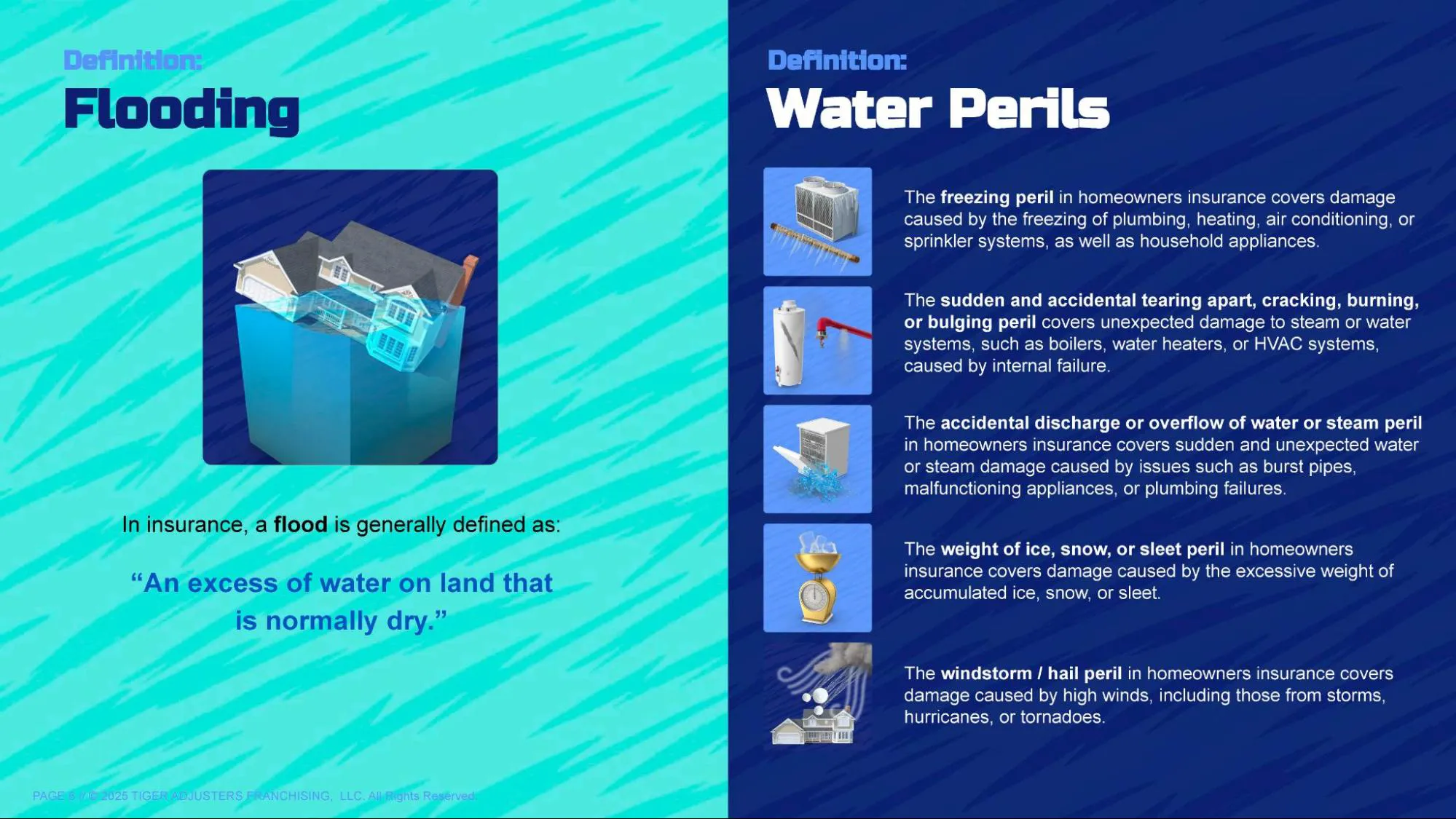

Within property insurance, a "flood” is generally defined as an excess of water on land that is normally dry, covering two or more acres of land or affecting two or more properties (one of which is yours). It typically involves rising water from natural sources like overflowing rivers, coastal storms, or heavy rainfall. This is distinctly different from other common water perils, such as burst pipes or accidental discharge within your home.

Let's talk about floods! This is super important, and trust me, you don't want to get this one wrong. When we talk about a "flood" in insurance terms, we're generally talking about water getting where it doesn't usually go – like covering land that's normally dry, or affecting a bunch of properties, not just yours. Think about big water, like rivers overflowing, or storms pushing ocean water onto land, or a massive downpour that overwhelms everything.

This is very different from your leaky faucet from 2008, or a burst pipe inside your house. Those are usually covered by your regular homeowner's policy, which is great! But floods? That's a whole other beast. It’s about making sure you know the difference between a puddle and a peril, because missing this detail can really soak your wallet!

Flood Insurance Purpose

How Flood Insurance Works

Standard homeowner's policies typically cover certain other types of water damage, like accidental discharge from a burst pipe, freezing of plumbing, or even damage from the weight of ice and snow. So, your general water problems inside are usually fine!

Bad news? Standard homeowner's, renter's, or condo policies do not cover flood damage. This is a crucial, widespread exclusion. If you live in an area prone to flooding, or even if you just want that extra layer of protection, you must purchase a separate flood insurance policy. It’s like they give you a super suit, but forget to add the waterproof seal. Good thing you have a Public Adjuster to act as your risk mapping specialist, helping you understand your specific flood risk and making sure you have all the necessary separate policies in place! Alarmingly, nearly 9 out of 10 homes with flood risk remain underinsured nationwide, leaving many vulnerable to significant financial loss.

No, definitely not! While the NFIP provides the majority of flood insurance, private flood insurance is also an option, and coverage details can vary.

Floods are a unique and often excluded peril from standard policies, so assuming you're covered by default can lead to catastrophic financial loss. Understanding the clear distinction between flood and other water damages is absolutely critical. For an accurate assessment of your specific flood risk and to confirm you have the right, dedicated coverage in place, call a Public Adjuster.